Did the White House just light the fuse of a financial crisis?

The war with Iran is causing oil prices to surge. Experts worry it’s the push of a domino that could break the global economy.

There is a narrow strip of water at the mouth of the Persian Gulf — just 21 miles wide at one point — called the Strait of Hormuz. I spent a whole lot of time thinking about it in graduate school. While you may not have thought much about it before this week, you should now. Your retirement and financial future might depend on that little waterway.

Amidst Trump’s sudden war, the Iranian regime has sealed off the Strait of Hormuz, holding a huge chunk of the world’s oil supply hostage. Nothing can pass through it without the threat of being blown up. Predictably, the price of oil is now surging. If there’s no resolution to the conflict — and oil keeps rising — the cost of everything else will go up, too (gasoline-powered vehicles move goods from A to B to C to you).

This could be what tips the world economy over the edge. In fact, it feels a lot like what happened in 2008, only in some ways, worse.

I don’t want to be alarmist, but I want you to understand how serious the situation is.

To be clear about the scale of what we’re watching, roughly 20 percent of the world’s oil passes through that waterway every single day, and despite threats of closure, the Strait of Hormuz has never been fully sealed off. During the Iran-Iraq War in the 1980s, both sides attacked tankers (the so-called “Tanker War”) and still the strait stayed open. While studying Middle East conflicts in graduate school, the Strait often came up. For Iran, it’s always been the ultimate geopolitical poker move. If they feel intimidated, they can remind everyone they have the ability to upend the economy.

Iran has threatened closure before, repeatedly, as a negotiating card. But it never played that card until now.

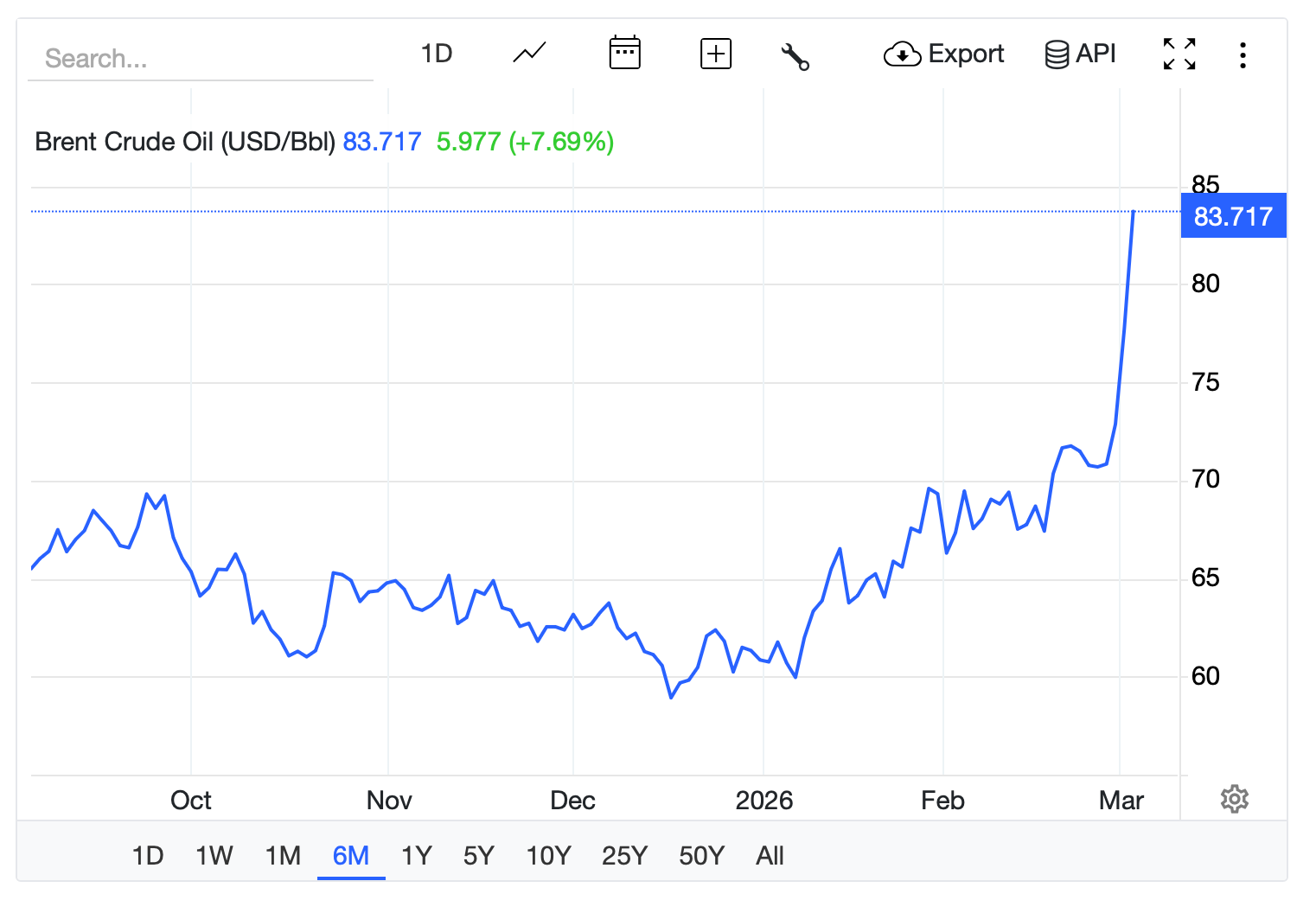

After U.S. and Israeli strikes against Iran that killed its leader over the weekend, Tehran has shut down maritime traffic through the Strait. At least 150 tankers are sitting at anchor nearby, going nowhere. Even if it were “open,” major shipping companies have halted transit across the Strait for fear that their ships will be blown up in the conflict. The result? Oil prices have surged more than $10 a barrel in a single week ($83 as of this writing) and are trending in the direction of a feared milestone: $100 per barrel.

Why is that such a feared milestone? Well, it’s the same threshold that oil breached in early 2008… when prices shot skyward… which led to the cost of goods going up worldwide… which then sent an already fragile economy spiraling into collapse.

In the short term, the market can absorb the shock because there are reserves worldwide. “Historically, geopolitical oil shocks fade quickly,” one Citigroup analyst noted this week. The word “historically” is doing a lot of work in that sentence. Indeed, history doesn’t have many examples of the world’s most critical oil chokepoint suddenly going dark.

Geopolitical observers have warned about it for many years, but we’ve never seen the moment actually come to fruition like this.

The critical variable here is time. If the disruption lasts only days, it’s just another “market event.” We’ll soon forget this spike ever happened. But if the disruption goes on for weeks — or even months — it could be something we don’t have a clean historical analogy for. In my personal estimation, the panic alone would be enough to set the global economy on fire, to say nothing of the actual increase in prices.

Here’s what people forget about 2008.

Everyone remembers Lehman Brothers, the global financial services firm that went upside down in 2008. It was a prelude to the mortgage collapse. But all those junk mortgages bundled together weren’t the only thing that sent the economy south. I like to think of the mortgages as the dry tinder. Oil was the actual accelerant.

In a matter of months, oil went from $90 a barrel to almost $150 a barrel, which was an all-time record, driven by a host of different factors. Interestingly, one of those factors at the time was Iran. While we weren’t at war with Iran in 2008, the fear of Iran building a nuclear weapon or starting a conflict pushed oil upward to levels that lit a fuse… before the financial crisis officially detonated.

Economist James Hamilton later concluded that if oil prices had not spiked in 2007-2008, the U.S. economy likely would not have entered recession when it did. The oil shock didn’t cause the collapse, per se, but it pushed an already teetering system to the edge. Then when Lehman fell, there was nothing left to catch it.

For whatever reason, I remember this better than most folks. Maybe it’s because I was driving a shitty, gas-guzzling car at the time. I was always at the pump. And I remember the numbers ticking up, as the news about the economy got worse and worse. I also remember that it felt a lot like it does right now. I was a student on a tight budget, grocery prices were going up, and everyone was already jittery about the economy. Feel familiar to you, too?

Remember: Oil doesn’t just raise gas prices. It raises the price of everything.

Petroleum is embedded in virtually every supply chain on earth. It moves all of our goods by truck, ship, and plane. When oil spikes, shipping costs spike, and there’s little that can be done about it. Then manufacturing costs spike and food costs spike. Every business that moves anything or makes anything or grows anything absorbs some part of the hit. Then they pass as much of it as possible onto consumers.

What that does, at scale, is erase “margin.” So for companies, that means they have thinner profits and have to institute hiring freezes or delay investment. For households, that means less money for everything else. You’re already experiencing this like me and my wife Hannah. As grocery prices have gone up, we’ve got less extra cash for other things in our lives. That’s a blinking red light.

It’s too soon to say whether this is a repeat of 2008. But I’ll be damned if I don’t warn you. It’s hauntingly similar.

Think of it another way. In 2008, the price of oil didn’t knock over all the dominos. It just nudged the very first one hard enough that when the housing crisis knocked over its dominos on the other side of the room, the two collisions merged into something catastrophic. Maybe a messy analogy. But what happened then (and now) is messy.

Now look at the dominos lined up already in 2026, in large part because of Trump’s gross mismanagement of the economy.

Consumer confidence is already cratering because everything is still so expensive. Although Trump tariffs have been struck down by the Supreme Court, he’s claiming other presidential powers to keep them in place — meaning goods will remain more expensive than they should be. Meanwhile, the federal deficit is exploding. And now, into that already fragile system, the Trump administration has introduced an oil shock by starting a war in the Middle East.

The chief economist at Moody’s Analytics, Mark Zandi, said it plainly this week:

“There is no economic upside to any of this, as the higher oil prices will weigh on growth and push inflation higher…This will, in turn, heighten Americans' affordability concerns and complicate the conduct of monetary policy, as the Fed will be unsure whether to respond to the weaker growth by lowering rates or to the higher inflation by raising rates.”

Translation: the emergency brake for the economy won’t work. It’s a “damned if you do, damned if you don’t” scenario for the Fed.

For now, all of this is hypothetical. I can’t say with certainty that Trump’s war with Iran will trigger the next major financial crisis. Hell, maybe Trump is telling the truth for the first time and intends for this to be a short and tidy little war that will wrap up just fine for everyone (except for the children who’ve died and the families of the U.S. servicemembers who’ve been killed and the people whose country will now become a power vacuum). Oil may slow down before it hits $100 a barrel.

But I’m not betting on a rosy outcome.

To me, the conditions look more dangerous today than they were in the summer of 2008. The kindling is a whole lot drier, and the accelerant is more flammable. Last time, there were a host of phantom factors driving oil prices up. This time, America has launched an actual war in the region that could drag on for months or more.

And unlike in 2008, the match wasn’t dropped onto the fuse by accident. It was struck deliberately by a president who was warned about the consequences, and started the war anyway.

Your friend, in defiance,

Miles Taylor

Thank you for your reporting, Miles. Your background/experience and current knowledge are invaluable. As someone who appreciates language well used, I appreciated this part of your post: “'Historically, geopolitical oil shocks fade quickly,'” one Citigroup analyst noted this week. The word “historically” is doing a lot of work in that sentence. Indeed, history doesn’t have many examples of the world’s most critical oil chokepoint suddenly going dark." Yes, that word, 'historically' is doing a lot of work. I plan to remember your wording because I think it may apply to many situations in the future. Again, thank you!

According to Zev Shalev, many in the Epstein network engineered and made money when the market crashed in 2008. Could we be watching an engineered crash? Let’s pay attention to who’s making money as a result of this war. Seth Abramson is coming out with a long relevent article later this week that should shed some light.